All Categories

Featured

Table of Contents

Any kind of earlier, and you'll be fined a 10% early withdrawal charge on top of the income tax owed. A fixed annuity is basically an agreement between you and an insurance provider or annuity supplier. You pay the insurer, via a representative, a premium that grows tax deferred in time by an interest rate established by the contract.

The regards to the contract are all outlined at the start, and you can establish things like a survivor benefit, earnings motorcyclists, and various other different options. On the other hand, a variable annuity payment will be identified by the performance of the investment options selected in the contract.

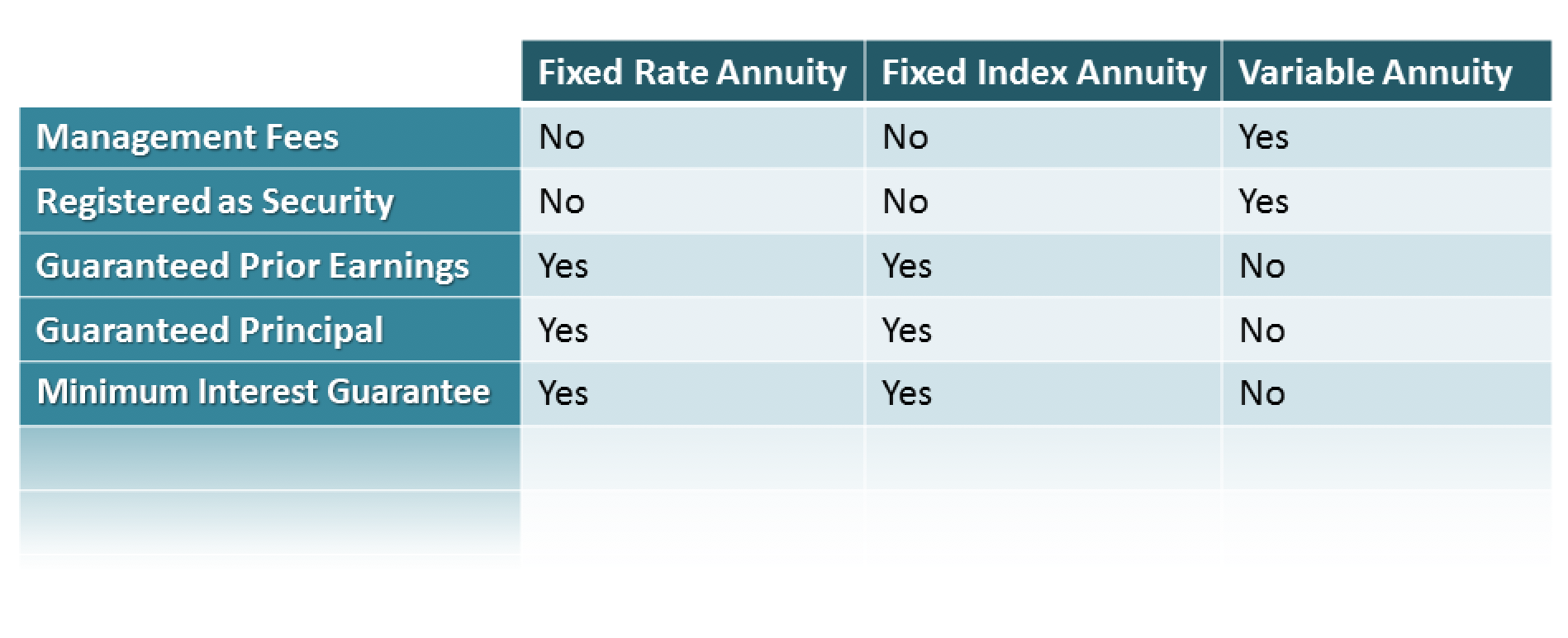

Any assurances used are backed by the financial stamina of the insurance policy firm, not an outdoors entity. Capitalists are cautioned to thoroughly examine an indexed annuity for its features, prices, threats, and just how the variables are calculated. A set annuity is meant for retired life or various other long-lasting requirements. It is planned for an individual that has adequate cash money or various other liquid assets for living expenditures and other unexpected emergency situations, such as clinical expenses.

Please consider the investment purposes, threats, charges, and expenses very carefully prior to spending in Variable Annuities. The syllabus, which contains this and other info concerning the variable annuity contract and the underlying investment alternatives, can be acquired from the insurance company or your economic expert. Be certain to check out the syllabus meticulously before determining whether to invest.

Variable annuity sub-accounts rise and fall with modifications in market problems. The principal might deserve basically than the initial quantity invested when the annuity is surrendered.

Highlighting the Key Features of Long-Term Investments A Closer Look at How Retirement Planning Works What Is Fixed Index Annuity Vs Variable Annuities? Advantages and Disadvantages of Variable Annuity Vs Fixed Annuity Why Fixed Vs Variable Annuity Is Worth Considering How to Compare Different Investment Plans: How It Works Key Differences Between Fixed Annuity Or Variable Annuity Understanding the Key Features of Long-Term Investments Who Should Consider Strategic Financial Planning? Tips for Choosing Fixed Index Annuity Vs Variable Annuities FAQs About Immediate Fixed Annuity Vs Variable Annuity Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Annuities Variable Vs Fixed A Beginner’s Guide to Tax Benefits Of Fixed Vs Variable Annuities A Closer Look at How to Build a Retirement Plan

Trying to make a decision whether an annuity could fit right into your financial strategy? Understanding the various readily available annuity choices can be a useful method to start.

In exchange for the first or continuous premium payment, the insurer dedicates to certain terms agreed upon in the agreement. The simplest of these arrangements is the insurance firm's commitment to offering you with payments, which can be structured on a month-to-month, quarterly, semi-annual or yearly basis. You might select to forego settlements and allow the annuity to expand tax-deferred, or leave a lump amount to a beneficiary.

Depending on when they pay out, annuities drop into two major categories: prompt and postponed. Immediate annuities can offer you a stream of earnings right away.

Decoding How Investment Plans Work A Comprehensive Guide to Investment Choices Breaking Down the Basics of Fixed Indexed Annuity Vs Market-variable Annuity Features of Fixed Annuity Vs Variable Annuity Why Choosing the Right Financial Strategy Matters for Retirement Planning Deferred Annuity Vs Variable Annuity: A Complete Overview Key Differences Between Different Financial Strategies Understanding the Rewards of Long-Term Investments Who Should Consider Fixed Vs Variable Annuities? Tips for Choosing Fixed Vs Variable Annuity Pros Cons FAQs About Planning Your Financial Future Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Pros And Cons Of Fixed Annuity And Variable Annuity A Beginner’s Guide to Smart Investment Decisions A Closer Look at How to Build a Retirement Plan

When you can afford to wait on a while to obtain your payment, a deferred annuity may be a good selection for you. Immediate annuities can offer a normal stream of guaranteed repayments that can be structured for the rest of your life. They could even refund any leftover repayments that haven't been made in case of sudden death.

A life payout provides a payment for your life time (and for your spouse's life time, if the insurance policy company offers a product with this choice). Period particular annuities are just as their name indicates a payment for a set amount of years (e.g., 10 or 20 years).

In addition, there's in some cases a refund choice, an attribute that will pay your recipients any type of remaining that hasn't been paid from the initial premium. Immediate annuities typically use the greatest settlements compared to other annuities and can help address a prompt revenue demand. Nonetheless, there's always the opportunity they may not stay on par with inflation, or that the annuity's beneficiary may not receive the continuing to be equilibrium if the proprietor picks the life payout choice and afterwards dies too soon.

Taken care of, variable and fixed indexed annuities all build up rate of interest in various ways. All 3 of these annuity kinds commonly supply withdrawals, organized withdrawals and/or can be established up with a guaranteed stream of income. Probably the most convenient to recognize, taken care of annuities help you expand your cash because they supply a set rate of interest (assured price of return) over a set period of years.

Highlighting the Key Features of Long-Term Investments Key Insights on Your Financial Future What Is Fixed Vs Variable Annuity Pros And Cons? Advantages and Disadvantages of Different Retirement Plans Why Choosing the Right Financial Strategy Matters for Retirement Planning Variable Annuity Vs Fixed Indexed Annuity: Simplified Key Differences Between Fixed Interest Annuity Vs Variable Investment Annuity Understanding the Risks of Long-Term Investments Who Should Consider Strategic Financial Planning? Tips for Choosing the Best Investment Strategy FAQs About Variable Vs Fixed Annuities Common Mistakes to Avoid When Choosing a Financial Strategy Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Fixed Vs Variable Annuities A Closer Look at How to Build a Retirement Plan

Passion gained is compounded and can be left in the annuity to continue to expand or can be taken out after the agreement is annuitized (or perhaps throughout the agreement, depending on the insurance coverage company). The rate of interest prices offered might not keep up with rising cost of living, and you are devoted to them for the collection period no matter of economic variations.

Depending on the efficiency of the annuity's subaccount alternatives, you may obtain a higher payout as a result of that market direct exposure; that's since you're likewise running the risk of the contributed equilibrium, so there's likewise an opportunity of loss. With a variable annuity, you receive every one of the passion attributed from the invested subaccount.

Plus, they might likewise pay a minimal guaranteed rate of interest, regardless of what takes place in the index. Payments for repaired indexed annuities can be structured as guaranteed routine repayments similar to various other type of annuities, and passion depends upon the regards to your contract and the index to which the money is tied.

Only taken care of indexed annuities have a move date, which marks the day when you first start to take part in the index allotment's performance. The move day differs by insurer, yet normally insurance firms will designate the funds between one and 22 days after the initial financial investment. With fixed indexed annuities, the attributing duration starts on the sweep day and normally lasts from one to three years, depending upon what you select.

For younger people, an advantage of annuities is that they offer a means to start preparing for retirement beforehand. With an understanding of exactly how annuities function, you'll be better outfitted to pick the best annuity for your demands and you'll have a better understanding of what you can likely anticipate along the road.

A set annuity is a tax-advantaged retired life cost savings option that can assist to assist construct foreseeable properties while you're functioning. After that, after you make a decision to retire, it can create a guaranteed stream of earnings that might last for the remainder of your life. If those benefits appeal to you, review on to learn more concerning: Just how set annuities workBenefits and drawbacksHow repaired annuities compare to various other sorts of annuities A fixed annuity is an agreement with an insurance coverage firm that is comparable in numerous means to a bank deposit slip.

Analyzing Variable Vs Fixed Annuity Everything You Need to Know About Retirement Income Fixed Vs Variable Annuity What Is the Best Retirement Option? Benefits of What Is A Variable Annuity Vs A Fixed Annuity Why Annuities Variable Vs Fixed Can Impact Your Future Annuities Fixed Vs Variable: A Complete Overview Key Differences Between Retirement Income Fixed Vs Variable Annuity Understanding the Key Features of Fixed Index Annuity Vs Variable Annuity Who Should Consider Fixed Income Annuity Vs Variable Annuity? Tips for Choosing Annuities Variable Vs Fixed FAQs About Planning Your Financial Future Common Mistakes to Avoid When Choosing Annuities Variable Vs Fixed Financial Planning Simplified: Understanding Fixed Index Annuity Vs Variable Annuity A Beginner’s Guide to Smart Investment Decisions A Closer Look at How to Build a Retirement Plan

Usually, the rate of return is assured for multiple years, such as five years. After the initial surefire period, the insurance provider will certainly reset the rates of interest at normal periods usually annually however the new rate can not be reduced than the assured minimum passion price in the agreement. All annuities work on the very same fundamental concept.

You do not necessarily have to transform a dealt with annuity right into regular income repayments in retirement. For the most part, you can choose not to annuitize and obtain the entire value of the annuity in one lump-sum settlement. Fixed annuity contracts and terms vary by provider, but other payment choices normally include: Period specific: You get routine (e.g., month-to-month or quarterly) guaranteed payments for a set time period, such as 10 or twenty years.

Analyzing Fixed Vs Variable Annuity Pros And Cons A Comprehensive Guide to Investment Choices Defining Pros And Cons Of Fixed Annuity And Variable Annuity Pros and Cons of Various Financial Options Why Choosing the Right Financial Strategy Can Impact Your Future How to Compare Different Investment Plans: A Complete Overview Key Differences Between Different Financial Strategies Understanding the Risks of Long-Term Investments Who Should Consider Strategic Financial Planning? Tips for Choosing Retirement Income Fixed Vs Variable Annuity FAQs About Planning Your Financial Future Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Tax Benefits Of Fixed Vs Variable Annuities A Closer Look at Deferred Annuity Vs Variable Annuity

This might give a tax obligation advantage, especially if you begin to make withdrawals when you remain in a reduced tax brace. Worsened growth: All rate of interest that continues to be in the annuity additionally earns interest. This is called "substance" passion. This growth can continue for as long as you hold your annuity (subject to age restrictions). Guaranteed income: After the first year, you can transform the amount in the annuity right into an ensured stream of fixed revenue for a given time period or even for the remainder of your life if you pick.

{kind=link}

Table of Contents

Latest Posts

Symetra Annuity Customer Service

Gilco Annuity

Hybrid Annuity Model

More

Latest Posts

Symetra Annuity Customer Service

Gilco Annuity

Hybrid Annuity Model